April 2022 - Market Update

The Month in Review is our monthly report providing economic commentary with Australian and global economic summaries, alongside market news for each key asset class.

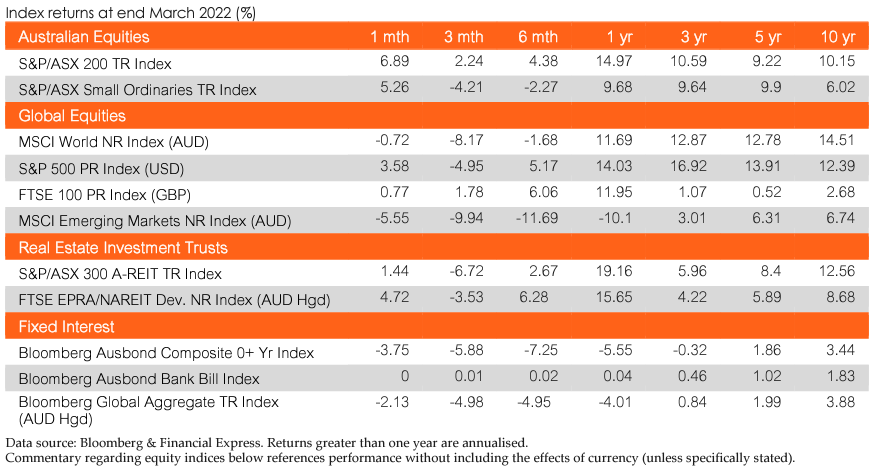

Australian equities

The Australian market closed out the quarter with the S&P/ASX 200 up 6.9% in March and all 11 sectors finishing positively. The Technology sector (+13.2%) led the index and rebounded from a February selloff, with Energy (+9.8%), Materials (+8.9%), Financials (+8.5%) and Utilities (+7.6%) all performing strongly.

The Energy and Materials sector continued their stellar year-to-date performances as commodity prices continued to soar. Meanwhile, Information Technology rebounded strongly from a perceived ‘bottom’ in February amidst rising interest rate pressures in overseas markets. However, volatility in this sector persisted given the uncertain macroeconomic backdrop. The Financials sector continued its sturdy performance as the major Australian Banks contributed to the strong Australian broad market performance. The S&P/ASX 200 finished the month within 2% of its August 2021 historical high. Overall, whilst the geopolitical issues in Ukraine remain a point of concern, Australian equity performance has been more robust than other markets with greater geopolitical risk.

In March, Momentum (+9.0%) and Growth (+7.2%) were the top performing factors. All factors performed strongly with Low Volatility (+3.8%) being the weakest factor. Over the past 12 months, Momentum is the top performer (+23.3%). Moreover, Shareholder Yield (-2.8%) has provided the lowest returns over the past quarter.

Global equities

Global markets continued their downward trend over the month of March as the Ukrainian conflict continued with no certain end in sight. Developed markets fared better than in February closing -0.9% lower by month end, Global small caps performed worse than their large cap counterparts closing with a -2.7% loss. Emerging and Asian markets loosely mirrored the return profile of the previous period, continuing to fall by -5.6% and -5.7% respectively.

Geopolitical uncertainty continues to be the core focus for investors as upward price pressure on energy and commodities hastens the pace of inflation across the globe. Momentum and quality factors were the best performers over the month returning 4.3% and 3.1% respectively, whilst equal-weighted and value factors were the laggards returning -0.7% and 0.4% respectively according to MSCI ACWI Single Factor Indices reported in local currency terms.

Property

March was a positive month for both the local A-REIT market and the broader Global real estate equities market with the S&P/ASX 200 A-REIT Index (AUD) and the FTSE EPRA/NAREIT Developed Ex Australia Index (AUD Hedged) advancing 1.25% and 4.99% MoM, respectively.

The strong monthly move in global REITs may be attributable to investors seeking higher income-producing assets that have the ability to keep pace with inflation. The S&P/ASX Infrastructure Index TR, comprising 9 constituents of the ASX300, advanced 6.81% MoM, equating to 8.87% YTD. The recent Federal Budget may provide a tailwind to the sector, with infrastructure spending announced that includes $17.9bn of road and rail as part of a $120bn 10-year infrastructure investment pipeline.

M&A activity during March across the A-REIT sector included Charter Hall (ASX: CHC) managed partnership with Dutch pension fund PGGM entering into a scheme implementation agreement to acquire Irongate Group, which will result in Charter Hall owning a 12% stake in the partnership. Additionally, Centuria Capital Group (ASX: CNI) formed a healthcare JV with Morgan Stanley Real Estate Investing which has been seeded with three healthcare real estate assets of $220m collective value.

CoreLogic reported that the national rental index increased by 1.0% during March to a total of 2.6% for Q1 2022, with national unit rents rising at a faster pace than houses. Growth in the value of the housing market has slowed in some major cities, with Melbourne and Sydney both recording negative numbers for March, -0.1% and -0.2% respectively (CoreLogic). Adelaide and Brisbane, however, tell a different story, both advancing strongly with 1.9% and 2.0% growth respectively (CoreLogic).

Fixed income

March saw Fixed Income markets deliver another poor result, a continuation of the trend throughout 2022 so far. With inflation remaining elevated across the world, central banks have begun to raise rates, most notably, in March the US Federal Reserve issued its first rate hike since COVID began. This has resulted in yields surging around the world, and Australia is no exception, with the 2- and 10-year yields of Australian Government Bonds increasing by approximately 70bps over the month. When combined with credit spreads which continued to widen, this resulted in the Bloomberg AusBond Composite 0+ Yr Index returning -3.8% over March, the worst monthly return in the indices history.

In the US, yields also rose across all durations, but the rate of increase was much higher at the short end of the yield curve, with 2-year yields increasing by 90bps compared to the 50bps increase in 10-year yields. This resulted in an inversion of the US yield curve, as 2-year rates surpassed 10-year rates, which some market participants have interpreted as a recessionary signal. The rapid yield increases internationally have resulted in the Bloomberg Barclays Global Aggregate Index (AUD Hedged) returning -2.1% over March, with currency fluctuations resulting in the unhedged variant returning -6.3%.

Economic News

Australia

Measures aimed at reducing strain on household budgets were announced in the Federal Budget, including a temporary cut in fuel excise and targeted rebates.

The RBA left the cash rate unchanged at 0.1% as widely expected. While mentioning that the war in Ukraine was a major new source of uncertainty, policymakers reiterated unpredictability over how persistent the pick-up in Australia's inflation on the back of recent developments in global energy markets and ongoing supply-side problems.

Retail sales increased by 1.8% in February, after a 1.6% gain a month earlier. February’s unemployment rate fell to 4.0%, which is the lowest jobless rate since August 2008, amid further easing of COVID-19 restrictions.

The Westpac-Melbourne Institute Index of Consumer Sentiment came in at 96.6 in March, below expectations of 99.2 and giving back some of the momentum from the 100.8 February result.

The NAB Quarterly Business Survey showed business confidence fell 5pts but remains elevated at +14 index points. Outside of mining, which saw a large increase in the quarter, confidence was softer in most industries, led by a decline in finance, business & property.

The S&P Global Composite PMI fell to 55.1 in March from 56.6 in February. Both manufacturing and service sector output expanded in March, driven by higher demand.

The trade surplus increased declined sharply to $7.46 billion in February, missing market forecasts of a surplus of %12 billion. This was the smallest trade surplus since March 2021, largely due to a surge in imports.

Global

Global Covid-19 cases continue to rise with numbers surpassing 485 million cases and 11 billion vaccine doses administered as at the end of March. A new Omicron sub variant emerged, causing a spike in infections across Europe and China, with China imposing targeted lockdowns in key provinces.

The Russian war on Ukraine continued to put pressure on energy prices, with Oil remaining volatile. Upwards of 4 million people have been displaced by the war with many fleeing to Poland and Germany. Inflation remains a concern, especially in the US and Europe, as it outpaces wage growth and puts pressure on household budgets.

The Federal Reserve lifted interest rates from 0.25% to 0.50% in March -the first rise in three years - as they look to tackle the highest level of inflation in years and leveraging off a strong US economy. Further near-term rises are expected, with the Fed anticipating rates to be in the range of 1.75-2.00% by years end.

Inflation climbed 0.8% in February, 10bps higher than anticipated, pushing the annual rate to a 40 year high of 7.9%. Allied to this rise in inflation, consumer sentiment dropped from 62.8 to 59.4 in March, the lowest reading since August 2011 PPI increased 0.8% in February, below market forecasts of 0.9%, while annual PPI matched market expectations of 10%, a level not seen since 1981.

Non-farm payrolls added 431,000 jobs in March, below the anticipated 490,000, whilst the unemployment rate dropped to 3.6%, below the anticipated 3.7%. Personal incomes grew 0.5% in February, flat on expectations and 40bps higher than the revised January figure.

The S&P Global Composite PMI rose to 58.5 in March as demand conditions and supply issues continued to improve from January’s Omicron impact.

The trade deficit remained steady in February at $89.2 billion, unchanged from the revised previous months result.

As widely expected, the European Central Bank kept interest rates at 0%, however it surprisingly sped up its asset purchase schedule for the upcoming months, noting that it could end in the third quarter if the medium term inflation outlook holds firm.

The inflation rate increased 0.9% in February, while the annual rate rose to a record high of 5.9%. Inflation is largely being driven by increasing energy prices.

Consumer confidence declined to -18.7, its lowest level since May 2020, dragged down by the war in Ukraine. Unemployment fell to a record low of 6.8% in February, down from the revised 6.9% in January but above the anticipated 6.7%.

The S&P Global Composite PMI fell from 55.5 to 54.5 in March as the economic impact of the war in Ukraine offset stronger demand for services as COVID-19 restrictions were lifted.

Retail sales rose 0.3% in February, below the 0.6% expected, with the annual rate coming in at 5.0%.

PPI rose to 5.2% in February, while the annual rate increased 31.4%, below the expected 31.4%.

In the UK, the Bank of England raised the base interest rate by 25bps to 0.75% in March, which is the third consecutive rise but in line with market expectations.

Inflation rose by 0.8% in February, ahead of an anticipated rise of 0.6% and ahead of the 0.1% contraction reported in January. The annual rate rose to 6.2% ahead of the expected 5.9%.

The unemployment rate dropped to 3.9% in January, below the anticipated 4% and is the lowest rate in two years.

Consumer confidence dropped to its lowest level in 16 months at -31 in March largely due to soaring living costs, interest rate hikes and higher taxation.

The PMI composite index came in at 60.9 in March, 1pt higher than February, with the services index growing 2.1pts to 62.60.

Retail sales fell 0.3% in February, well below the anticipated 0.6% rise, and bringing the annual rate to +7%.

PPI came in at 0.8% in February, missing the anticipated 0.9% and bringing the annual rate to 10.1%.

China's CPI grew by 0.6% over February, 30bps higher than expectations whilst the annual rate was flat at 0.9%, as anticipated.

The unemployment rate was 5.5% in February, up from 5.3% in January and while the highest jobless rate in a year, was in line with the government’s “no more than 5.5%” target for the year.

The Caixin China General Manufacturing PMI fell to 25-month low of 48.1 in March 2022 from February's reading of 50.4, missing market consensus of 50. This contraction came amid measures to contain the COVID-19 outbreaks and export sales dropping at the fastest pace in 22 months.

The Caixin Composite PMI fell from 50.1 in February to 43.9 in March, well below the anticipated 49.0.

Retail sales increased 0.3% in February, bringing the annual rate to 6.7%.

A resurgence in COVID-19 cases resulted in targeted lockdowns in key cities and regions, including Shanghai and Shenzen, threatening more global supply chain disruption.

The Bank of Japan left its key short-term interest rate unchanged at -0.1% and the 10-year bond yields around 0% during its March meeting, by an 8-1 vote, as widely expected.

Japan’s GDP grew 1.1% over the fourth quarter of 2021, with the annualised rate improving from -2.8% to 4.6%, undershooting expectations by 30bps and 100bps, respectively.

Japan's annual inflation rate rose 0.9% in February, the most since April 2019, after a 0.5% gain a month earlier.

Japan’s unemployment rate dropped 10bps to 2.7% in February, better than the anticipated 2.8%.

Retail sales declined 0.8 % in February, with the yearly rate also falling 0.8% against the anticipated 0.1% fall.

Tokyo’s population fell in 2021 for the first time in more than a quarter of a century, with a net loss of 48,592. This follows concerted efforts from other cities and prefectures to attract new residents with business loans and lower cost of living.

Currencies

The Australian dollar continued to climb in the month of March closing 3.4% higher relative to the greenback and 4.9% in trade-weighted terms. The period experienced the widest high-low range of the year thus far at 3.6 cents (previous high in January 3.5 cents). Rising commodity prices continued to be the primary driver of AUD support over the month of March, albeit some domestic support was provided through better-than-expected February employment figures.

Disclaimer: This document is for the exclusive use of the person to whom it is provided by Lonsec and must not be used or relied upon by any other person. No representation, warranty or undertaking is given or made in relation to the accuracy or completeness of the information presented in this document, which is drawn from public information not verified by Lonsec. Financial conclusions, ratings and advice are reasonably held at the time of completion but subject to change without notice. Lonsec assumes no obligation to update this document following publication. Except for any liability which cannot be excluded, Lonsec, its directors, officers, employees and agents disclaim all liability for any error or inaccuracy in, misstatement or omission from, this document or any loss or damage suffered by the reader or any other person as a consequence of relying upon it.

Copyright © 2022 Lonsec Research Pty Ltd (ABN 11 151 658 561, AFSL No. 421445) (Lonsec). This report is subject to copyright of Lonsec. Except for the temporary copy held in a computer's cache and a single permanent copy for your personal reference or other than as permitted under the Copyright Act 1968 (Cth), no part of this report may, in any form or by any means (electronic, mechanical, micro-copying, photocopying, recording or otherwise), be reproduced, stored or transmitted without the prior written permission of Lonsec.

This report may also contain third party supplied material that is subject to copyright. Any such material is the intellectual property of that third party or its content providers. The same restrictions applying above to Lonsec copyrighted material, applies to such third party content.